The impact on the security business in 2012

|

December 2012 |

[an error occurred while processing this directive] |

| Mergers,

Acquisions & Investments The impact on the security business in 2012 |

|

| Articles |

| Interviews |

| Releases |

| New Products |

| Reviews |

| [an error occurred while processing this directive] |

| Editorial |

| Events |

| Sponsors |

| Site Search |

| Newsletters |

| [an error occurred while processing this directive] |

| Archives |

| Past Issues |

| Home |

| Editors |

| eDucation |

| [an error occurred while processing this directive] |

| Training |

| Links |

| Software |

| Subscribe |

| [an error occurred while processing this directive] |

Summary

Merger and acquisition activity declined in 2012 by 27% but we forecast that it will return to its historic high of 2011 by 2017. The structural changes that are now taking place across the physical security industry will bring about more strategic acquisitions from within. The VCs have shown that they are much more confident of investing in the physical security industry, whilst major companies from the ITC and Defense industries continue to make forays into the security industry. We believe that in 2013 we can expect a mega-merger between two of the larger security players. These companies have with the rare exception not acquired any significant business in the last three years. That said, a mega merger is more likely to happen next year than it has for some time and the general prospects for growth through acquisition look a lot more promising.

Internal Strategic Acquisitions

In the last four years M&A activity has for the most part been

driven

through strategic buys, within the security industry to acquire or

leverage new technology and move into horizontal product businesses in

order to provide total solutions, and / or improve focus on particular

vertical markets where demand is fast growing.

Strategic buys within the industry have been the main driver for consolidation in 2012 but its impact is down on 2011 and this trend may well continue as companies from the ICT and Defense business and Private Equity Companies make further forays into the security industry.

The proportion of

external buys has increased and in 2012

accounting for 30% of the total acquisition business measured by

volume. Consolidation in 2012 has therefore been more influenced by

external companies buying into the physical security market than in the

previous three years whilst conversely the internal players,

particularly

the major conglomerates have decided to abandon growth through

strategic mergers and acquisitions in the last two years.

With the exception of Tyco and Stanley, none of the incumbent major

conglomerate suppliers made any significant acquisitions in 2011 or

2012. This is very surprising given the volume of M&A deals

transacted during this time increased on previous years.

In our 2011 report we identified that the single most important trend in M&A activity in that year was the growth in acquisition of biometric and identity assurance solution technology companies. This trend has continued in 2012 accounting for 24% of all deals completed this year. The application of this technology is very important to the growth of Access Control but is by no means the only application to embrace the need for improved identity security.

Cross Border Transactions

Cross border transactions continue to be a strong feature of the

consolidation process. Over the last two years exposure to US markets

has

become a strategic priority for a number of European companies. For the

first eight months of this year the notable acquisitions by European

companies in the US include Assa Abloy’s purchase of LaserCard to

incorporate within its HID operation, Identive Group (German / US)

purchase of idOnDemand, and Kaba’s purchase of e-Data.

Gradually over

the next five years we expect that most activity under this

dynamic will centre on Asia and particularly China where rules on

ownership have been significantly relaxed in recent times. In December

2010, Infinova floated on the Chinese Stock Market and realised a much

higher valuation than it would in the western world. The market thought

that more companies would take up this option but so far no have. China

Security & Surveillance Technology (CSST) however did delist on

Nasdaq (reported to be unhappy with its valuation) and privatized. The

Chinese stock market is very volatile and indeed Infinova’s value has

fallen sharply since it floated.

External Buys – ICT & Defense

Related Companies

[an error occurred while processing this directive]Defense,

IT and communications companies have over the last three years

bought into the security industry. The initial flurry of activity has

reduced somewhat in the last six months as they digest and take stock.

We expect them to resume their interest in the business both through

acquisition of product and system suppliers and through alliance.

Defense expenditure is likely to decline across the western world

during the next five years and the security industry provides an

expanding

market and a way of leveraging their high technology base.

So expect these transformational deals from the Defense and IT and

Communications businesses, to gain further traction in 2013 and beyond.

M&A Activity Declines in

2012

Merger and acquisition activity has grown by a compound annual rate of

15% in the first ten years of this millennium but during this time it

peaked and declined twice. In the last three years it has completed

another

cycle of rise and fall. External more than internal forces have had

most influence in creating this volatility.

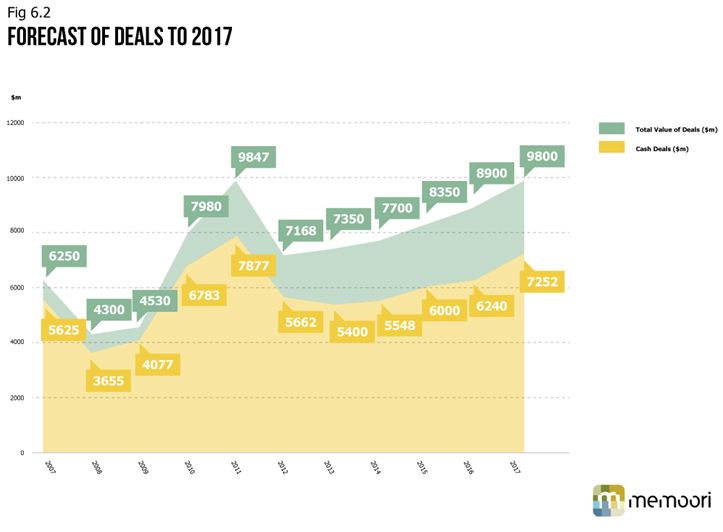

Fig 6.2 shows that the value of merger and acquisition deals in 2011 was $9.847 billion a rise of 23% over the previous year which was a record high, but in 2012 it declined to $7.168 billion a fall of 27%. So why has the love for growth through acquisition cooled off in 2012?

There are two main reasons for this. The first is that the industry has

undergone major consolidation and restructuring during the last five

years

and is now catching breath, and the second is the lack of confidence by

the traditional major conglomerates to commit more investment to the

industry.

These two factors alone would have caused a much greater reduction in acquisition activity than 27% but for the increased activity in the middle market, mainly populated by specialist security companies. The decline in the volume of deals in 2012 was only 15% and this reflects the fact that in 2011 a number of mega deals over $1 billion were completed. This is a remarkable performance given the economic crises that the industry has had to ride through and the fact that most of the major conglomerates have not had the confidence to go for growth through merger and acquisition in the last three years.

So to conclude, 2012 has been a good year for acquisition activity

particularly considering that poor economic trading conditions have

reduced the confidence to spend big, but nevertheless this industry has

fared better than most.

Forecast of M&A Business

to 2017

We forecast a steady annual growth rate of 6.5% over the next five

years to 2017. This assumes that the European debt crisis will find a

long term solution and at least stabilize the EEC economy but not

provide any growth until the last quarter of 2013. Whist the US will

grow at around 2% and emerging markets will maintain their 2012

performance.

This the 4th Edition of our Annual Report “The Physical Security Business in 2012” goes on to detail the Performance of Exit Multiples 2005 – 2012, analyses why Strategic Buys Dominate and IPO’s & MBO’s Disappoint, why M&A Should Play a More Important Role in the next five years and reviews the State of the Investment Business & its Exposure to the Security Industry.

For more details visit the Website, http://memoori.com/physical-security-2012

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The Automator] [About] [Subscribe ] [Contact Us]