|

July 2013 |

[an error occurred while processing this directive] |

|

What Every Building Owner Should Know About Open Systems and Smart Buildings |

Brian Turner, President, Controlco |

| Articles |

| Interviews |

| Releases |

| New Products |

| Reviews |

| [an error occurred while processing this directive] |

| Editorial |

| Events |

| Sponsors |

| Site Search |

| Newsletters |

| [an error occurred while processing this directive] |

| Archives |

| Past Issues |

| Home |

| Editors |

| eDucation |

| [an error occurred while processing this directive] |

| Training |

| Links |

| Software |

| Subscribe |

| [an error occurred while processing this directive] |

Building automation systems are one of the key ingredients to reducing

the energy consumption in building and facilities, yet they are

increasingly difficult to manage and program. There are many challenges

to maintaining these systems and there is growing pressure to integrate

these systems with other building systems to create a “smart building.”

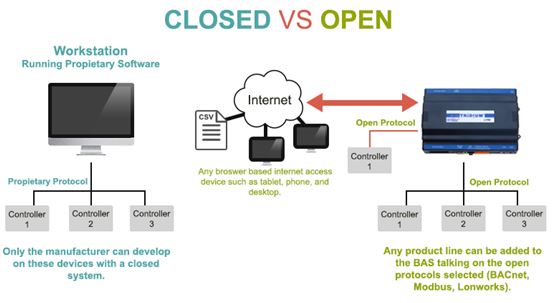

The traditional building automation systems (BAS) business model

consists of products and systems that are hamstrung with proprietary

protocols and tools, forcing all service, support and upgrade work

through a single authorized contractor in the local market. This

results in artificially inflated costs to the building owner as there

is no competitive market from which to procure these services. In

addition, proprietary technology forces the owner to only purchase

spares and replacements from the original vendor (typically) at

inflated rates and prevents the owner from taking advantage of

technological advances and integration to other products that may be

available from different vendors. As a result, building owners have

been forcing the market towards more and more “open systems”.

Traditional BAS vendors however have been slow to give up their

inflated profit margins under the traditional model, and as a result

are obscuring the message of what it means to be truly open.

Building owners, not typically experts in automation systems, are

increasingly confused with the messaging around open systems for smart

buildings and Building Automation Systems. Unfortunately this confusing

messaging is often presented by the automation manufacturers

themselves, thus containing substantial credibility. The market largely

accepts open communication protocols as a substitute for open systems.

This can lead to a lot of frustration when owners are expecting their

new “open system” to integrate with other systems within the building

or other buildings within a campus or portfolio environment.

There are many ways to score systems relative to compatibility at the

protocol level. BACnet, LonWorks, Modbus, OPC and other commonly used

network protocols have documented standards that must be met in order

to carry the label, but this is only 20% of the open system story.

While it is the foundation of the story, and arguably the most

important piece, focusing on the protocol alone can leave a building in

the same position that proprietary systems did in the 1990’s. This is

the exact problem that pushed the market to demand open protocols, and

the sharp rise of integration platforms like the Niagara Framework™ by

Tridium.

We believe that we have developed a simple mechanism for scoring

whether a system is truly open or not. Our system assigns one point for

achieving an “open” score in each of the following categories:

Protocol, Programming Tools, Product Availability, Local Service

Contractors, and User Interface Technology. The max possible score

achieved is five points. Don’t get discouraged; most manufacturers will

not score five points today.

Protocol

As mentioned earlier, the protocol is the foundation of the open

system. There are, however, many layers within the network architecture

where the system may or may not meet the requirements of the open

protocol. Some products in the market expose certain points to the open

protocol, while others stay behind and communicate only via the private

proprietary protocol unless specifically exposed to the open protocol.

This can create many issues when attempting to integrate to an

enterprise solution or when attempting to access setpoints or control

parameters when running analytics or fault detection algorithms.

It is important to clearly understand and articulate the requirements

of the building for the life of the control system; which can last 20

years or longer, specifically when selecting building automation system

controls, lighting control systems, and access control systems. For

example, if the requirement is that every field device must support

BACnet schedules and BACnet trends, a system whose field devices do not

support those functions would not get a point for this category.

Scoring:

1 Point if the system supports an open protocol at the level required.

0 Points if the system does not support an open protocol at the level required.

Programming Tools

The programming tools are often used by manufacturers to make a system

100% proprietary even though the communication protocol is 100% open.

This is where the biggest challenge for the building owner starts. Many

of the manufacturers who fall into this category focus a lot of

attention on the protocol and are heavy supporters of open building

standards. They do this knowing full well their products are rarely, if

ever, part of a truly integrated solution. The market pressure to

commoditize products and make smart building products open conflicts

directly with the history of manufacturers whose primary goal is to

build product dependence in the building.

If the programming tool is not open and is not available for purchase

on the open market, it is probable that the building will not have much

choice for service, upgrades, or long term service.

Scoring:

1 Point if the programming tools are available for sale to the market and if factory training is offered to service contractors

0 Points if the tool is only available to Authorized Integrators and Building owners who have purchased a control system.

Product Availability

Manufacturers have several channels in the US market available to

deliver product. The most common channels are manufacturer branch

offices (direct), system integrators who purchase product direct from

the manufacturer (1-Step), and distributors (2-Step). With rare exception, manufacturer branch offices sell and support a

proprietary control system that is only available from the branch

office. Some of the devices sold may be sold in other channels, but

there is generally a product that excludes others from competing with

the branch office in the local market. There are many reasons for this,

meant for another category.

System integrators often resemble the branch offices in the way they go

to market. Typically, there is only one per market and their charter is

to build market share for the brand they represent. There is often an

exclusive territory granted in exchange for brand loyalty.

Unfortunately, this can have negative consequences for the owner in

many ways. In some cases there are multiple system integrators

representing the same brand in the same market, but this provides

owners with false security since the integrators are not authorized to

compete against one another.

Distributors who represent control systems are typically more

engineering and technology focused than the parts wholesaler that

immediately comes to mind. They represent one or more brands and work

with controls contractors, system integrators and mechanical

contractors to serve the market. This can be incredibly powerful when

the right mix exists in a market.

Scoring:

1 Point if there are multiple competing system integrators in the market or if there are one or more distributors in the market.

0 Points if the channel is branch office or exclusive system integrator

Local Service Contractors

The goal of this category is to determine the availability of service

contractor within a 30 mile radius of the desired end-user location(s).

This can often be confused with the last category since the presence of

multiple system integrators in the market should equal multiple service

providers. That is not necessarily the case, since many of the system

integrators focus on new construction and design build construction

markets. They can have little or no service departments.

Scoring:

1 Point if there are two or more competing service contractors in the local market.

0 Points if there are fewer than two competing service contractors in the local market.

Visualization / User Interface

The way people are expected to interact with the system is the final

point in the tally. It is common for systems to require a computer

whose primary purpose is to provide access to the building automation

system or lighting control system. Most of the time, buildings are

saddled with multiple machines dedicated to the disparate systems in

the building.

[an error occurred while processing this directive]

The best way for customers to visualize the information in a smart

building is via a common web browser using one or more types of

devices. The users of open systems should expect to access these

systems using the same tools they access their banking information or

purchase products. This should be out of the box functionality for

systems claiming to be part of a smart building, but sadly, it is not

for the majority of systems. All is not lost, however, since more

manufacturers are hearing this message and are working toward a

solution.

Scoring:

1 Point if a common web browser on any device is the user interface technology.

0 Points if java applet, flash client, or other proprietary technology is required.

Manufacturer Brand Identity

This category may or may not be important building owners. It is worthy

of considering, but not worth a point. Many building owners are looking

for long term brand identity. This category is extremely subjective,

but none-the-less can carry some weight when making the decision.

Perceived risk may also play a role here given that the larger more

established brands are likely to be supported for the life of the

building control system and beyond. There is little certainty, these

days, where technology advances so quickly.

Why should Building Owners Care?

The demand for cost savings from reduced energy use and operational

efficiency in conjunction with the need for more automated intelligence

in the building means there will be a demand for more fully integrated

“smart buildings.” As technological advances, it is easier to collect

and store more data than ever before. Products that optimize operations

through systems integration, machine to machine (M2M) communication,

and data analytics are now a reality. As it is exponentially more

difficult to integrate systems that score low on this scale, the

requirement for owners to truly adopt open systems is not only

important to immediately reduce operational costs through open

competition, but to future proof themselves as the integrated “smart

building” becomes the rule as opposed to the exception.

About the Author

Brian Turner is President at Controlco, an enterprise system integrator

and value added distributor headquartered in Oakland, CA. Brian has

passion for the integrated facilities business and looks forward to a

day when smart building systems achieve their potential in running

energy efficient and operationally efficient facilities.

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The Automator] [About] [Subscribe ] [Contact Us]