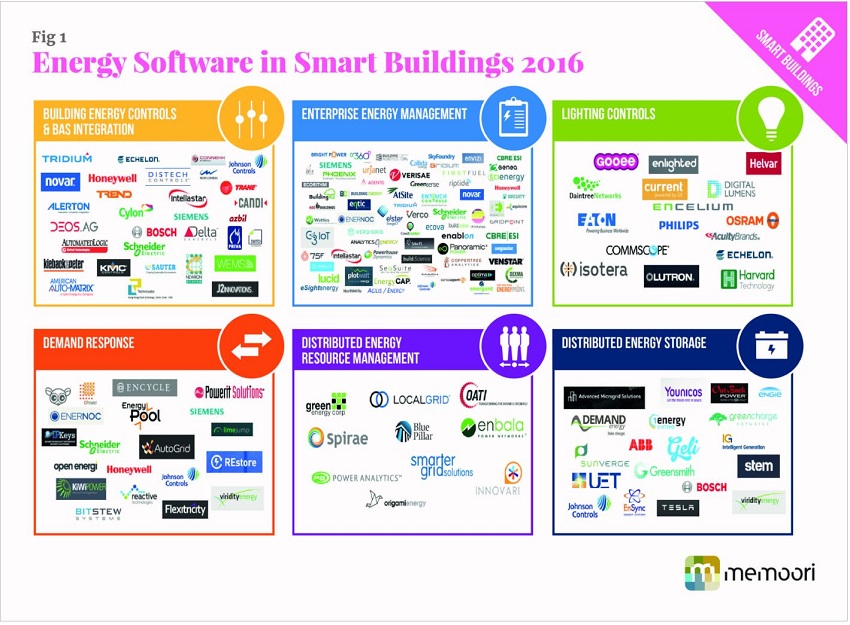

The building performance software industry has at least 350 established suppliers delivering across six main different market segments that can be further sub-divided into 16 segments.

James McHale,

Managing Director,

Memoori

|

March 2017 |

[an error occurred while processing this directive] |

| The Transformation of the Building Performance Software Business The building performance software industry has at least 350 established suppliers delivering across six main different market segments that can be further sub-divided into 16 segments. |

James McHale, Managing Director, Memoori |

| Articles |

| Interviews |

| Releases |

| New Products |

| Reviews |

| [an error occurred while processing this directive] |

| Editorial |

| Events |

| Sponsors |

| Site Search |

| Newsletters |

| [an error occurred while processing this directive] |

| Archives |

| Past Issues |

| Home |

| Editors |

| eDucation |

| [an error occurred while processing this directive] |

| Training |

| Links |

| Software |

| Subscribe |

| [an error occurred while processing this directive] |

The

building performance software industry has at least 350 established

suppliers delivering across six main different market segments that can

be further sub-divided into 16 segments. These segments overlap and

cause confusion when the building operators are evaluating how they

meet their value propositions.

This is particularly critical now that the

major real estate owners are in the midst of investigating the impact

of the Building Internet of Things (BIoT) on their building estates.

Memoori’s recent report The Market for Building Performance Software 2016 to 2020

investigates the shape and structure of the market and identifies the

measures that are being made by the BPS industry to meet this challenge.

The report has focused on some 358

well-established companies who are providing software to commercial and

industrial buildings, split into six main categories as shown in the

table below. We have not included all the companies that are part of

the Real Estate & Property Management Software within the

definition sector of CRE Tech which some reports estimate at 2,200.

This includes software for lease management, accounting and other

specific real estate administrative functions, which is not within the

scope of our report.

ENERGY SOFTWARE PROVIDERS

The

major BAS suppliers still dominate here, but they have lost market

share over the last 10 years. They have the largest customer base and

heritage estate and more recently have expanded their offerings by

means of strategic acquisitions and alliances and are no longer reliant

on BECS Supervisory Software.

GE will become a formidable competitor to

the BAS vendors in the not too distant future, as Current rapidly

expands into the building automation sector.

EEMS providers account for the majority

share of this listing accounting for 28% of the total number of

software suppliers. A multitude of vendors are competing for a slice of

the energy management solutions market which can be broken down into

three distinct camps:

Companies

targeting specific market verticals such as Telkonet, which targets the

hospitality sector, Vigilent, which targets data centers and Joulex,

which was focused on IT and data center infrastructure, have been able

to carve out a slice of the market with their highly targeted

offerings. Joulex’s success caught the eye of Cisco, who snapped up the

emerging player in a November 2013 acquisition deal.

On the IT front, major players including

IBM, HP, SAP, and Oracle are increasingly incorporating energy

management functionality and / or interface capabilities into their

platforms.

PHYSICAL SECURITY & FIRE DETECTION SOFTWARE SUPPLIERS

There

are many companies focusing on one specific sub-category (VMS, Video

analytics, PSIM, PIAM, Fire detection, Access control, Mass

notification) which are detailed in the report. The major

manufacturers, such as Bosch, Tyco, United Technologies, Siemens, and

Honeywell offer software across the range of fire and security

solutions and in some cases, covering the complete suite of building

performance software.

[an error occurred while processing this directive]One

company to watch is Bosch, who has been very active in developing their

software capability in recent years and are prominent in the

development of IoT capability. Although their initiatives are heavily

targeted towards the manufacturing sector, their security systems,

energy and building technologies business are a focus too.

Bosch Software Innovations have also

recently been partnering with Zumtobel, an architectural lighting

company in the development of IoT-connected lighting solutions at the

Life Cycle Tower Building in Dornbirn, Austria. The Zumtobel lighting

system is linked to Bosch’s cloud-based IoT suite, which allows for

real data insights, the basis for new value-added services in the areas

of predictive maintenance or condition monitoring for building

operators and facility managers.

With considerable capability and resources

across energy management, fire and security and facilities management,

Bosch is likely to build its expertise quickly in these areas and may

challenge the incumbent BAS providers in providing building performance

software solutions across all disciplines.

REAL ESTATE AND PROPERTY MANAGEMENT SOFTWARE SUPPLIERS

Real

Estate and property management software providers accounted for over

26% of our listing which focuses on the major suppliers. The major

players offering a range of software for this sector include Accruent,

Archibus, Planon and IBM. Some 500 companies offering software for real

estate and property management have entered the sector in the last five

or six years. Realcomm estimates that there are 2,200 companies in the overall CRE tech sector.

This will be a continuing feature of the

sector, even with a high degree of acquisitions, new entrants are able

to offer software, due to low entry barriers.

This article was taken from our recent report “The Market for Building Performance Software 2016 to 2020”

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The Automator] [About] [Subscribe ] [Contact Us]