Smart

Building Synergy

Through

Building Energy Management Systems and Enterprise Energy Management

Software

|

November 2013 |

[an error occurred while processing this directive] |

|

Smart

Building Synergy

|

| Articles |

| Interviews |

| Releases |

| New Products |

| Reviews |

| [an error occurred while processing this directive] |

| Editorial |

| Events |

| Sponsors |

| Site Search |

| Newsletters |

| [an error occurred while processing this directive] |

| Archives |

| Past Issues |

| Home |

| Editors |

| eDucation |

| [an error occurred while processing this directive] |

| Training |

| Links |

| Software |

| Subscribe |

| [an error occurred while processing this directive] |

Both Building Energy Management Systems (BEMS) and Enterprise Energy

Management (EEM) have major parts to play in delivering Distributed

Energy and Demand Response services connecting across Smart Buildings

and Smart Grid. This reinforces that together they can also reach

across associated applications. This must be synergy personified.

Integrating the technical services in buildings is not a new

development but more recently advances in technology together with the

need to reduce CO2 emissions from buildings has spurred on demand and

opened up new business opportunities. Memoori’s new research report

“The Market for BEMS and EEM 2013 to 2017”

” seeks to establish how this will develop, and together how they will

achieve more than the sum of their parts when they are fully

integrated, not just interfaced; delivering more benefits and a better

return on the clients investment.

There is no doubt that through alliance, acquisition and integration;

these two separate businesses will play a vital role in maximizing

energy conservation in buildings whilst generating income and reducing

operating costs.

BEMS Market Sizing Data & Business Development

We estimate that the world sales of BEMS at installed prices was $15.6

billion in 2012 and we forecast that by 2017 it will have reached $23

billion. The figures are based on the total installed value and include

all controllers, valves actuators and sensors and supervisory software.

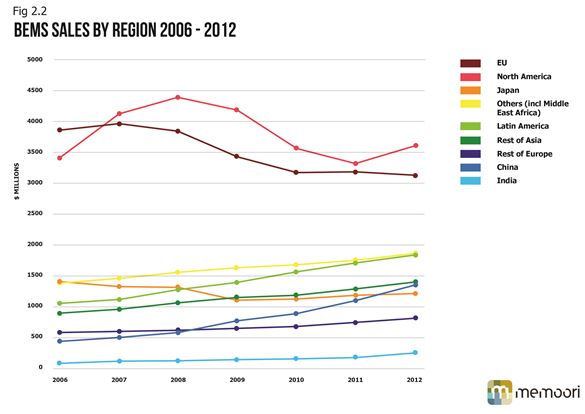

The largest market is North America with a share of 23.27% followed by

the EU at 20.25%. Demand in North America and the EU declined in 2007

and 2008 respectively as the construction of new buildings declined.

The BEMS market in North America returned to growth in 2012 and the EU is forecast to stabilize in 2013 and then return to growth in 2014. Asia will deliver the highest rates of growth. China and India are the fastest growing markets and they are expected to sustain current growth rates of around 18% to 2017. Latin America and the Middle East are forecast to grow at CAGR of 8% from 2013 to 2017.

This business is well established and dominated by 4 major

companies. However the channels of distribution have changed over

time and this has brought about better opportunities for the smaller

players as the reduction in direct sales to the end user has declined.

Open systems is putting Supervisory Software developed and maintained

by BEMS companies under pressure from outside sources and the medium

sized players struggle to keep up to date. Software is not their forte.

But the major challenge for BEMS suppliers is that their business is

morphing into the much wider Enterprise Energy Management (EEM)

business and at the same time interfacing with Smart Grid and they need

to accommodate this.

EEM Market Sizing Data & Business Development

The two major prongs of the EEM business lie in making Smart Buildings

much smarter and the Smart Grid fully ADR right across the transmission

and distribution network by providing a real time analysis of supply

and demand. These two markets alone have the potential to spend upwards

of $225 billion by 2030 with Smart Buildings looking the more

attractive and robust business because it will be funded by the private

sector and an attractive ROI can almost be guaranteed. The US market

for EEM solutions is estimated to be $6 billion in 2012, and could grow

to $15 billion by 2020.

The last decade has seen EEM develop from provided a specific energy

domain service delivering a data aggregation and consolidation service

to an enterprise scale service providing cost reduction and energy

efficiency applications in Smart Buildings. The more sophisticated

software package can deliver optimal energy solutions across all facets

of energy supply, consumption, conservation and total emissions control

in single, multi-buildings and multi-sites, across different countries.

Growth is being driven by the need to meet CO2 emissions in the low

carbon economy and large multi-national corporations are seeking

solutions to provide an enterprise view of energy use and associated

costs that can also be implemented across multiple facilities. This is

not a “one size fits all” solution as vertical markets by building type

have different needs and priorities in addition to vendor preferences.

We therefore expect that the Smart Building sub markets will be

targeted by type of vertical building. However EEM companies need to be

able take the data from the BEMS and this is where, for retrofitting

existing buildings, they will need to extract and join data from BEMS

systems that operate on different communication protocols.

Fundamental Structural Changes are Underway

Leading BEMS companies have massive heritage estates and are amongst

the world’s major Energy Service Companies (ESCOs). They are therefore

in a strong position to help EEM suppliers get a foothold in the Smart

Building Market. However BEMS suppliers and ESCOs are also intent on

taking a piece of the EEM business.

Although not particularly well known for their prowess in EEM, they

have been acquiring companies with this expertise for the last five years.

BEMS / ESCO companies active here include Johnson Controls, Honeywell,

Schneider Electric, Siemens and ABB. They are the world’s leading

suppliers across both businesses and the last three are also leading

international suppliers of Smart Grid products and services.

[an error occurred while processing this directive]

At this time they don’t have the software technology to build platforms

for major projects but Schneider Electric recently signed a strategic

technology agreement with one of the world’s major software companies,

OSIsoft. OSIsoft will provide their PI System, an infrastructure

technology for the management of real-time data and events whilst

Schneider Electric will provide comprehensive energy management

control.

The major EEM companies have the capacity and capability to deal direct

with the owners of very large Smart Building real estates and they will

have contact with sources that will influence the buying decision on

EEM purchases. These companies will be targeting comprehensive EEM

systems in Smart Buildings.

EEM will bring about a sharp evolutionary change to the building

services and management business because the buyers demands will

require a high level of commercial and technological expertise that is

not yet honed by many of the suppliers. To acquire these skills they

will require alliance and partnerships between the various groups of

players and across the vertical markets. Those that grasp the

opportunity will be rewarded with a highly profitable and fast growing

business.

More details on Memoori’s report can be seen here - http://www.memoori.com/portfolio/bems-market-2013-to-2017/

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The Automator] [About] [Subscribe ] [Contact Us]