Energy Efficiency Cleantech

Solutions

What Happened? - Part 1

What Happened? - Part 1

Chip Pieper,

VP Business Development

Ezenics, Inc.

|

September 2012 |

[an error occurred while processing this directive] |

|

Energy Efficiency Cleantech

Solutions

What Happened? - Part 1 |

Chip Pieper, VP Business Development Ezenics, Inc. |

| Articles |

| Interviews |

| Releases |

| New Products |

| Reviews |

| [an error occurred while processing this directive] |

| Editorial |

| Events |

| Sponsors |

| Site Search |

| Newsletters |

| [an error occurred while processing this directive] |

| Archives |

| Past Issues |

| Home |

| Editors |

| eDucation |

| [an error occurred while processing this directive] |

| Training |

| Links |

| Software |

| Subscribe |

| [an error occurred while processing this directive] |

Most of us have

noticed contraction in the adoption of energy

efficiency related solutions of late. From venture capital firms

focusing their investment strategy on sectors other than cleantech, to

start-ups folding, to slow acceptance of larger controls companies' “state

of the art” platform offerings, to acquisitions that fail to deliver

significant value or differentiation in the market. Something seems to

be going on in our industry. If companies were adopting solutions on a

widespread-scale, we obviously wouldn’t be experiencing such a

contraction.

Rather than speculate what the root causes are that are impacting

adoption, I believe it all boils down to decision-making. Why do

companies buy or don’t buy?

Those of us, who provide solutions to the market with what we believe

are strong value propositions, often prescribe on the basis of guesses

and assumptions. That is, we prescribe before we diagnose what the client’s true needs are

and their criteria for making decisions. Realizing that companies

have to conduct their business with less resources (time, people,

money) than they did previously, I thought it would be interesting to

gain the perspective of both the providers of solutions and those who

consume it, as it relates to energy efficiency cleantech adoptions.

In an effort to achieve decision-making nirvana, I felt it was

necessary to interview at least 25 different people/companies across

industries (big box retail, industrial manufacturing, hospitals,

government, commercial real estate management, large software companies

and a large insurance company with many real estate holdings) that

“consumed” energy efficiency solutions. Everyone I spoke with had the

ability to strongly influence or make decisions regarding adoption for

their organization. As such, each interviewee was first asked one

simple question to start the discussion, “What are the top three

constraints or issues impacting your organization’s ability to adopt

energy efficiency solutions?”

In addition, I also interviewed a number of “providers” of energy

efficiency solutions to try and understand what they saw were the

leading issues that slowed or even prevented the adoption of their

solutions. The organizations represented were varied and included

cleantech software companies, venture capital firms, controls/hardware

manufacturesr, utilities, integration companies, and commissioning

firms.

To be clear though, this was a qualitative study not quantitative.

There’s absolutely NO scientific evidence that could be

considered

statistically significant. Matter of fact, everyone I interviewed had

the ability to define energy efficiency solutions in their own words as

it related to their company. Furthermore, rather than attempt to gain

approval to use names of companies, individuals and quotes, I thought

it would be more beneficial to have an open and honest discussion off

the record. Thereby removing all doubt that this undertaking was indeed

like a box of chocolates – you never

know what you’re going to get.

Nevertheless, what surfaced was telling and shared across verticals, as

well as with both consumers and providers.

As I mentioned earlier, the first question asked was simple, “What are

the top three constraints or issues impacting your organization’s

ability to adopt energy efficiency cleantech solutions?” Even though

each interviewee represented different verticals, there were

similarities worth exploring. Here are the top seven most recurring issues

or constraints that “consumers” experienced:

| 1. Lack of “qualified people” to either hire or outsource the business to. |

| 2. Experienced and qualified employees were seen as the difference maker in maximizing energy efficiency solution success. However, they need to be continuously skilled up/trained on these new solutions/technologies and this was viewed as a constraint. |

| 3. Some employees fear being displaced by technology and in certain cases, end up circumventing the solution and severely impacting its success. |

| 4. Energy costs are flat in most geographies. |

| 5. Lack of 3rd party validation or “case studies” supporting the proposed solution. Where has the solution worked and what were the results. |

| 6. The inability to deliver on promised results i.e. 20% Energy Savings! The perception was that much of what is being “sold” is just hype. |

| 7. Finally to my surprise, Life Cycle Costs were deemed more relevant in making the final decision than a two year ROI. |

In the case

qualified talent, many consumers felt providers could do a

much better job of offering more competent technicians to deliver the

necessary services. Even though virtually all consumers wanted to

consider their providers as strategic partners and invite them into

their “inner circle,” they often felt put off by the lack of

professional expertise. Some even discontinued services on the basis of

“misaligned resources.” Keep in mind; the majority of consumers I

interviewed were from fortune 500 companies, large hospitals, and big

government.

Nonetheless, “intelligent

boots on the street” seems to be the consumer

objective, when it comes to people and process. An “agile” motivated

technician, who embraces technology, accepts change and welcomes the

opportunity to be continuously educated on maximizing the business’

investments in energy efficiency solutions, appears to be the desired

model. Isn’t that every employers wish? As it turns out, reality is

quite different. An inability to attract qualified employees, and

provide growth opportunities that map back to compensation and

professional status seems to be a major constraint for the majority of

consumers I spoke with. Contrast that occurrence with a “perceived”

threat of energy efficiency technology solutions displacing current

employees - you subsequently have opposing forces working against each

other.

Nonetheless, “intelligent

boots on the street” seems to be the consumer

objective, when it comes to people and process. An “agile” motivated

technician, who embraces technology, accepts change and welcomes the

opportunity to be continuously educated on maximizing the business’

investments in energy efficiency solutions, appears to be the desired

model. Isn’t that every employers wish? As it turns out, reality is

quite different. An inability to attract qualified employees, and

provide growth opportunities that map back to compensation and

professional status seems to be a major constraint for the majority of

consumers I spoke with. Contrast that occurrence with a “perceived”

threat of energy efficiency technology solutions displacing current

employees - you subsequently have opposing forces working against each

other.

One angle we could consider regarding talent

is the convergence-taking

place in our industry. According to consumers, IT is playing a much

bigger role in the adoption of energy efficiency solutions and their

involvement on multiple levels, certainly impacts decision-making. As

such, let’s take a page out of their history book. Can you remember the

IT guy back in the day? He sported a custom-made pocket protector,

comb-over, high waters, and some “busted up” glasses. Furthermore, he

had the office next to “Boiler Room Bob”. What happened? Where did the

IT guy go?

One angle we could consider regarding talent

is the convergence-taking

place in our industry. According to consumers, IT is playing a much

bigger role in the adoption of energy efficiency solutions and their

involvement on multiple levels, certainly impacts decision-making. As

such, let’s take a page out of their history book. Can you remember the

IT guy back in the day? He sported a custom-made pocket protector,

comb-over, high waters, and some “busted up” glasses. Furthermore, he

had the office next to “Boiler Room Bob”. What happened? Where did the

IT guy go?

Though there were a few major “accelerants” that were responsible for

IT’s transformation and ascendance to the C-Suite, one significant

agent of change that propelled IT’s explosive growth in the 90s was

compensation. Apart from the fascination and draw of high tech, what

really attracted top talent was the opportunity to receive strong

salaries, excellent growth potential, and of course “cashing-in” on the

success of the business. Unfortunately, the energy efficiency

sector is pretty much devoid of these qualities. Apart from VC-backed

cleantech start-ups, rarely do people run to this industry in an

attempt to make serious coin and cash-out.

Even though the energy efficiency sector briefly experienced a similar

transformational “accelerant” which attracted investment, talent, and

growth potential, the sector has flattened out most recently. According

to consumers, much of this is due to empty promises of “significant

savings” and overblown hype. “Perceived Reality is Reality” has run its

course. The consumer has spoken, they want proof that these solutions

can surface the suggested value claimed by providers.

These empty claims of significant

savings have not only contributed to

the flattening of cleantech adoption, it has also led to many Venture

Capital firms focusing their attention on other investment options,

rather than cleantech. This is due primarily to start-ups overselling

their solution, “empty promises,“ little returns or worse yet, little

hope of any returns for their investors. This all affects

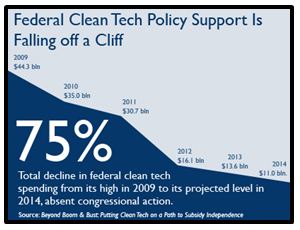

innovation, and its impact is systemic. Coupled with the fed’s

reduction in cleantech incentives, stoking the business motivations for

speculative growth are missing some of the accelerants they once had to

propel their desire to transform a chronic industry problem into a

cleantech solution.

These empty claims of significant

savings have not only contributed to

the flattening of cleantech adoption, it has also led to many Venture

Capital firms focusing their attention on other investment options,

rather than cleantech. This is due primarily to start-ups overselling

their solution, “empty promises,“ little returns or worse yet, little

hope of any returns for their investors. This all affects

innovation, and its impact is systemic. Coupled with the fed’s

reduction in cleantech incentives, stoking the business motivations for

speculative growth are missing some of the accelerants they once had to

propel their desire to transform a chronic industry problem into a

cleantech solution.

To further complicate matters, 3rd party validation in the form of

industry case studies plays a significant role in the decision-making

process. If we’re talking about innovative energy efficiency

technologies, providers better have some type of proof that their

solution works, repeatedly, in a similar consumer enterprise

environment.

Many consumers I spoke with were pretty troubled with the lack of

providers’ case studies in which a specific consumer was willing to

state publically that a solution was effective in surfacing measurable

value and were capable of a strong return on investment. Obviously,

there are numerous innovative energy efficiency solutions available in

the market, which have delivered significant value for consumers.

Unfortunately, we just do not have enough “deep” case studies

throughout the industry that enable the “enterprise consumer” to

comfortably say yes to adoption on the basis of “claimed” energy

savings alone.

Here’s the kicker though. One of the biggest obstacles “providers”

stated as a constraint was, you guessed it, the consumers’ willingness

to provide case studies. Very few consumers were willing to detail

their experiences publically. Not only is “quality people” an issue in

opposition, it turns out that 3rd party verification is as well. We’ll

explore the later impasse in more detail in our next issue.

Additionally, the notion that consumer’s only buy on a two year ROI is

misleading. Although every single consumer I spoke with all stated

money was ALWAYS an issue, never ONCE did a two year ROI play “the

dominant” decision-making criteria (as claimed by many providers). Life

cycle costs were deemed much more relevant for this consumer sample.

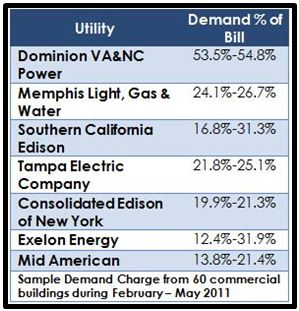

Compounding matters even more was the

issue of energy costs. As

my colleague Kelsey Haas mentioned in her AutomatedBuildings.com

article last month, “in the last 5 years, electricity consumption

charges have decreased, but demand charges have significantly risen in

both cost and percentage of the monthly utility bill. The

increase in demand charges on the monthly utility bill is not always

obvious to consumers as taxes and other line item charges that were

once based on kWh are now based on the monthly peak kW instead.”

Compounding matters even more was the

issue of energy costs. As

my colleague Kelsey Haas mentioned in her AutomatedBuildings.com

article last month, “in the last 5 years, electricity consumption

charges have decreased, but demand charges have significantly risen in

both cost and percentage of the monthly utility bill. The

increase in demand charges on the monthly utility bill is not always

obvious to consumers as taxes and other line item charges that were

once based on kWh are now based on the monthly peak kW instead.”

[an error occurred while processing this directive]Therefore

as consumption charges have appeared to flatten, the

relevance of efficiency solutions has taken on a new appearance. Those

consumers that view energy as a low cost expense have eased off on

their consideration for cleantech solutions that provide energy

efficiency. However, those consumers that have experienced the pain

associated with higher demand charges were taking measures to deploy

services that addressed this opportunity.

Conversely, the issue of energy savings was rarely the “dominant

decision-making driver” in adopting energy efficiency cleantech

solutions. Although energy savings were certainly an objective, it

appeared to be other more pressing consumer needs, which drove

decisions such as comfort, maintenance, extending equipment life,

labor, and process improvement. We’ll discuss this in more detail is

next month’s Part 2 edition.

Even though there were many other points that consumers brought up in

our discussions, the top seven mentioned above were clearly the most

repeated constraints that I heard throughout my conversations. In next

month’s installment we’ll explore what the prevailing sentiment is

among the providers of energy efficiency solutions. What do they see

are the constraints impacting the adoption of cleantech solutions on a

more widespread scale? And finally, we’ll tie both consumers and

providers together with what appear to be opportunities for “coming

together” more effectively.

Please stay tuned.

[an error occurred while processing this directive]

[Click Banner To Learn More]

[Home Page] [The Automator] [About] [Subscribe ] [Contact Us]